CORRUPTION, LAWYERS, CHARITIES, CHURCHES, NON PROFIT CORPORATIONS

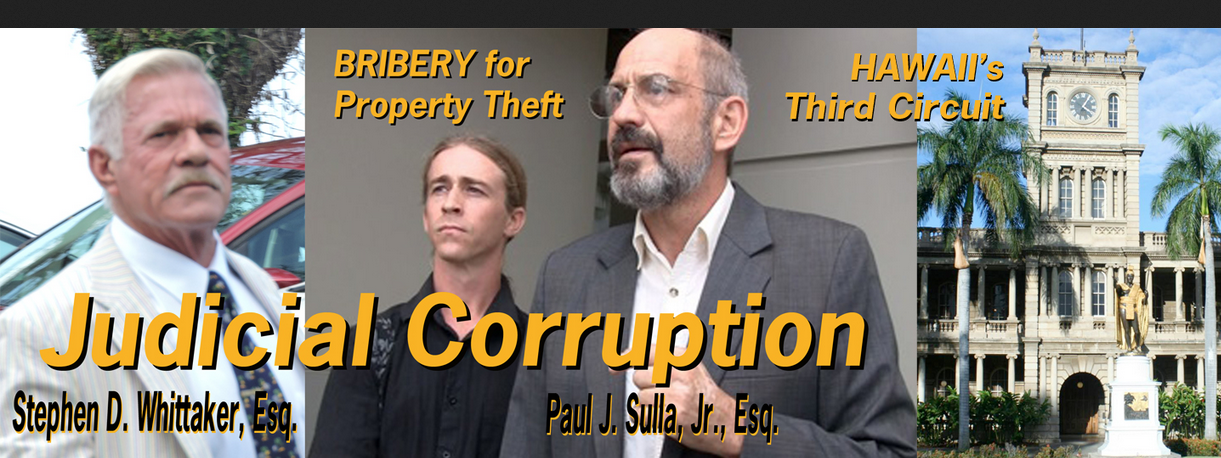

Big Island Co-counsel Stephen D. Whittaker and Paul J. Sulla, Jr. set Jason Hester (middle) up with a sham “church” to defraud the State, the courts, and unwitting victims.

(Excerpted, Edited, and Supplemented on 10-21-16 from Original Posting on 12-27-15 by Codefore)

“The Charity Scam” or “Guess where your money went?”

Creating a trust fund to hold and manage your money can be beneficial when done for the right reasons and by a competent honest lawyer. But there can be a down side to this carrot. The downside is that your lawyer must be trustworthy because once the lawyer moves your money from your bank or investment fund, you may no longer have absolute control of the funds and then become vulnerable to theft.

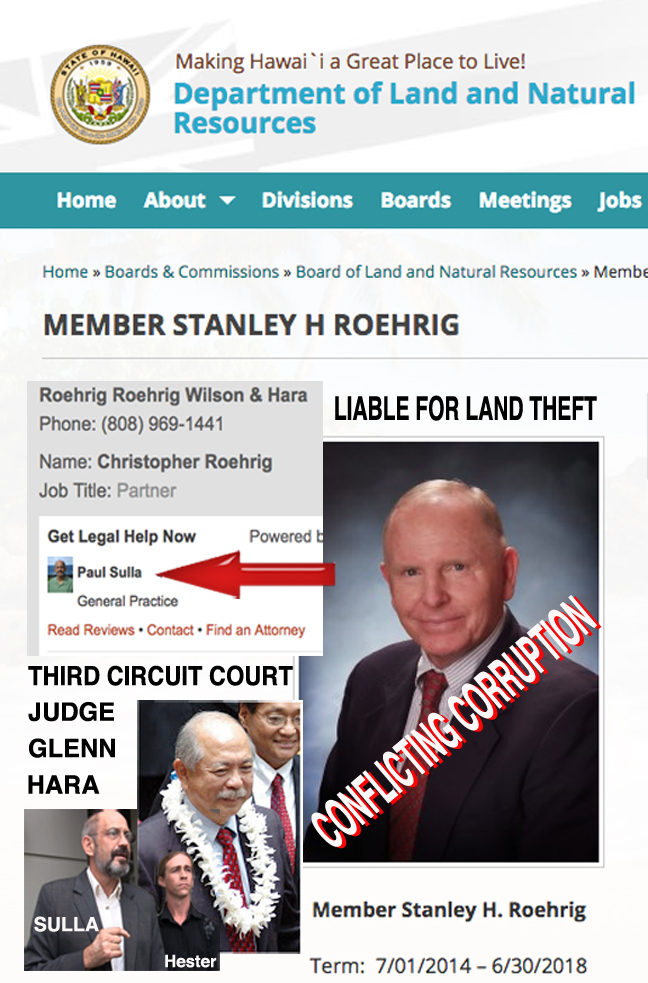

A classic case of this can be read here: Miyashiro v. Roehrig, Roehrig, Wilson and Hara, Hawaii Intermediate Court of Appeals, 2010.

Its not easy to locate an honest attorney. Creating a trust can be beneficial but attorneys who do not reveal existing connections or associations with so called “charities,” or legitimate non-profit charitable corporations, are usually up to NO GOOD!

Their associations are sometimes a maze of closely woven complicit criminals–non-profit corporations, banks and people in the local government who scratch each others backs in the search of innocent victims. They actually conspire to steal your funds.

Corrupt lawyers know how to convince and steal your money without leaving evidence that they did anything illegal, except point you in the wrong direction. That’s assuming you are still alive after the trust is in place. Lots of times they arrange for your death.

The modus operandi of these lawyers is to contact wealthy people and sell them on the idea of protecting their money from the Federal Government tax system.

The lawyer pictured above, Paul J. Sulla, Jr. is a classic example of this. Read this one of several in which he was indicted, but was permitted to go free: USA v Ong: Order Denying Defendant Arthur Lee Ong’s Motion for Acquittal; March-6-2012. See also: USA-v-Bruce-Robert-Travis-Disqualitication-of-Sulla.

Establishing a trust in good faith is a good idea for many people, and is not always illegal, but the non-profit or charity business is not always what it says it is, or appears to be.

Just because “charities” are legally designated as “non-profit,” or are religious corporations doesn’t mean they are not able and willing to steal. These corporations are not well regulated, and all too often the non-profit, non-taxable Federal and State laws benefit and enable unscrupulous lawyers and their clients to enrich themselves unjustly.

Charity laws make it possible to move millions of dollars from the gun sights of the IRS into the accounts of non-profit and or charitable corporations. The non-profit law in itself enables lawyers to steal and hide your money.

The common denominator of all of these scams are banks. Stolen funds cannot be “washed” without the use of bank accounts. Banks are the first step to change the money from legal possession to illegal possession.

A victim’s money must be diverted from the victim’s bank into an account controlled directly by either the attorney, or an organization that is controlled, or “friendly” with, the attorney such as a living trust.

Usually when this happens, the transfer of money is also the transfer of ownership. The formation of a living trust, or regular trust, can mean that a new owner (lawyer or trust) is now in control. A competent lawless attorney would never have his/her name on the first bank account stepping stone (that would be illegal). So instead, your money is put in the name of one corporation, or even transferred to a second trust or corporation, and possibly even a third entity before individual names surface out of the fog of corporations.

Case Study in Non-Profit Sector Corruption

It is alleged that Hawaii Attorneys, Nancy Budd, Katherine Lloyd, Paul Sulla Jr., and Joe Moss are examples of Hawaiian trust attorneys who have personally benefited (at their direction) from the distribution of funds to non- profit charitable corporations and non-profit corporations, or to other non-profit organizations who they are either directly or indirectly associated with them.

The alleged plan for these funds is to eventually line their pockets in the form of cash, gratuities such as car rentals, exotic trips etc. These are all “perks” that may be rewarded to them for locating, and eventually transferring, money into the bank accounts controlled by their colleagues in the charity business.

Hawaii seems to be a hotbed for this mischief. In the case of lawyers Stanley Roehrig and Glenn S. Hara, the court found that they had made off with George Miyashiro’s stocks (in Miyashiro v. Roehrig, Roehrig, Wilson and Hara, Hawaii Intermediate Court of Appeals, 2010.) Paul Sulla, in Hilo, is alleged to have transferred financial interests from one client’s trust money into “shell” companies owned or operated by him. He left a paper trail that is highly incriminating. Either he was not sophisticated enough to hide his direct receipt of other peoples funds, or considered himself “untouchable,” or both.

Local banks may have investment opportunities and legal departments available to their clients. Sometimes they unwittingly or knowingly refer their customers to consulting lawyers who have conflicts of interest. Corrupt bankers in bed with lawyers turn blind eyes to their history of complaints, fraudulent activities. The payoff is great, because they have colleagues who sit on the boards of directors of the banks used to hold and leverage the money.

In Kauai, where I performed an in-depth investigation, here’s how it worked:

Attorney Katherine Lloyd worked as legal counsel for the First Hawaiian Bank, and so did lawyer Nancy Budd. First Hawaiian Bank has their own numerous trust corporations, and when people deposited large amounts of money in this bank, they were candidates for the formation of trusts to “protect” their money in ways that the Bank legally cannot. Lloyd leveraged this situation by referring the actual creation of a bank customer’s living trust to her colleague Nancy Budd. Or Nancy Budd may have been retained as an adviser for the client, and recommended the use of the First Hawaiian Bank.

Budd drew up the Trust, named an executor to control the trust, named another attorney colleague as the executors adviser (on the trust payroll), and recommended a “charity” to hold an interest in the trust such as the Hawaii Community Fund.

Lloyd also worked for Hawaii Community Fund, until a conflict of interest complaint was made. Then she resigned.

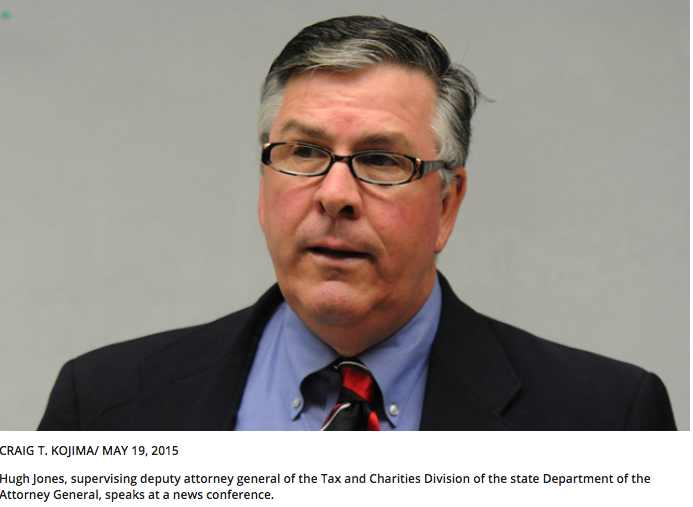

To make things much worse for the client, and great for Lloyd, her husband is Hugh Jones who just happens to be the State of Hawaii’s official investigator for non-profits’ fraud and crime! Jones, who was arrested for drunk driving in September, 2016, works for the Hawaii Attorney General’s Office, in their Trust and Charities Department. When a conflict of interest complaint was made to the Hawaii Attorney Generals office by one of Lloyd’s victims, Jones neglected the problem. He also denied he had anything to do with the business of his wife, Lloyd. And he also said she was innocent of any wrong doing.

To make things much worse for the client, and great for Lloyd, her husband is Hugh Jones who just happens to be the State of Hawaii’s official investigator for non-profits’ fraud and crime! Jones, who was arrested for drunk driving in September, 2016, works for the Hawaii Attorney General’s Office, in their Trust and Charities Department. When a conflict of interest complaint was made to the Hawaii Attorney Generals office by one of Lloyd’s victims, Jones neglected the problem. He also denied he had anything to do with the business of his wife, Lloyd. And he also said she was innocent of any wrong doing.

Hugh Jones did the same thing with another victim on the Big Island who reported attorney Sulla to Jones, for committing a similar non-profit scam resulting in the theft of his house by Sulla.

Many Cases Involve Murders

And some of these cases involve alleged murders. Once the trust is in place, in at least two cases investigated by Codefore, the trust contributor (retiree who possessed the original funds) unexpectedly died. The assets were immediately liquidated and funds deposited into a living trust where the administrators distributed the funds to themselves, other trusts, or charities.

In a case involving Lloyd and Budd, the first deposit of liquidated funds went into the First Hawaiian Bank and the American Savings Bank. Conveniently, the CEO of the Hawaii Community Fund is on the Board of the American Savings Bank. Surviving relatives either received a small fraction of the trust (inheritance) or received nothing. Two of the survivors claimed that the Living Trust had been altered after the deceased’s death.

And the police department can also be involved in these scams. The Kauai Police Department, for example, had possession of the Lloyd/Budd trust that none of them had ever seen before. The Kauai PD claimed they took the “Living Trust” from the deceased home for “safe keeping.”

And the police department can also be involved in these scams. The Kauai Police Department, for example, had possession of the Lloyd/Budd trust that none of them had ever seen before. The Kauai PD claimed they took the “Living Trust” from the deceased home for “safe keeping.”

In answer to these allegations, Ms. Budd stated ” I can tell you in no uncertain terms that there was nothing illegal or unethical done with respect to my representation of Mr. ……….. (or any client, for that matter). His children’s inheritance was not “taken from them illegally,” and I want to be clear that any such suggestion they have made to you is false.”

In another case investigated by Codefore, attorney Paul Sulla Jr. represented a seller in the sale of valuable property in Pahoa, Hawaii. Unfortunately, in this case, it was the property seller who died before the deed to the property could be transferred to the new owner. It is alleged that Sulla impersonated the seller, who was on his death bed in Arizona, not Hawaii, when Sulla is alleged to have conspired with the Third Circuit Court notary, forged a couple of signatures, and later filed a new deed to the property.

But Sulla’s deed was not to the new purchasers, but was to a Trust created and controlled by Sulla days before the seller’s death.

Then, to doubly mask his liability, Sulla claimed the property had never been paid for, and he auctioned it off through a fake “church” Sulla created.

All of this information came out in a civil court of law, in front of a Circuit Judge who apparently didn’t think that Sulla had violated any criminal laws. The purchasers are still trying to either get their money back, or the deed to the property.

Money Laundering Through Charities

An example of a money laundering structure is indicated in the below schematic. This chart is the exact chart used for legal purposes to explain how trust funds become invisible, that is “washed”.

In some cases the elderly are led to believe that a trust will insure that their surviving relatives will benefit after death by implementing a so called “living trust.” Little do they know that once the money is in the newly formed trust, or these attorney’s “favorite” non-profit charity, their money may be out of the grasp of the Federal Government, but is now under control of non-profit organizations that that “wash” the money by moving it back and forth until there is no “paper trail” leading to the actual distribution. The money is then distributed, and is usually not distributed to the poor, or to charities who do charitable business. The “SALON” news organization says this:

“Another way the wealthy avoid paying taxes on their billions is to make charitable donations. If you donate property, you never have to pay income tax on that donation, whatever it costs you and how much it’s worth right now. Well you might say, at least someone benefits from the charity. Whether or not the charitable donation is a scam in whole or in part depends on the answer to that old question: qui bono? Aka, who benefits? That’s where the real scam takes place.”

“And there’s no legal requirement that a charity must spend its wealth. In fact, IRS rules require only that charities spend about 5 percent of their investment assets annually, and all or part of this amount can be spent on salaries and “expenses,” rather than devoted to the charitable purpose the charity purports to be serving. So, what happens with a charitable trust, set up by a billionaire, and controlled by one of the billionaire’s children? The child gets a job and a salary for life. Maybe a mansion to live in and entertain in as a fringe benefit. This is a great gig for the heir.”

A case in point is the “Hawaii United Way”–a charitable non-profit corporation that receives money from a central clearing house charity known as the “Hawaii Community Foundation.” A look at their “Annual Reports” only list assets and contributions.

The 2015 Hawaii Community Foundation disbursements appear below, and I am not sure what these figures really imply, since their report simply says that this is their “Position:”

- Donor Grants 2.7 Million

- Scholarships 4.5 Million

- Partner ships 8.2 Million

- Donor advised grants 12.5 Million

- HCF initiatives ??? 7.3 Million

- Other Foundations: 7.3 Million

- Other Grants: 4.1 Million.

The United Way might well be listed in “Other Foundation” or “Partnerships” on the Hawaii Community Foundation, but they most certainly received cash from the Hawaii Community Fund as the HCF is listed as a contributor on the United Way web site along with a list of approximately 30 other charitable organizations that the United Way either received money from or donates money to. And each organization has a staff and Board of Directors that presumably all receive money for their time. The United Way tax returns can be viewed on the internet at: https://www.auw.org/financial-information

–End–

Related Articles and Videos

Hawaii Ballistic Missile Threat: Was 38 Minutes of Terror a Simple “Mistake” or PSYOPS?

Deep State Drops Nuclear PSYOPS on Hawaii Irradiating the Planet

I-Preditors Exposed in Troll Triad

Hawaii Senator Roz Baker Caught in Bribery Scandal with Pfizer/Monsanto Lobbyists

Journalists Expose Political Cover-up of Judicial Corruption in Hawaii

Dope Paradise Godfathers Secretly Block Justice From Hawaii To Control The Global Colony

RSS